Most payment mistakes around events do not happen during the show. They happen afterwards, when the stage is cleared, visitors have gone home and the administrative rush begins: paying artists, closing supplier invoices, reimbursing crew and sometimes processing hundreds of refunds. In that moment, an outdated company name, a typo in an IBAN or a changed bank account on an invoice can create delays, manual work or fraud risk.

For event organizers, being able to check an IBAN by name is therefore not a small administrative detail. It is a practical safety layer in the payment workflow. Especially with bulk payments, it is not enough to know that an IBAN is technically valid. You need to know whether the account belongs to the party you are about to pay.

Why the IBAN-name combination matters

After an event, payments often arrive in clusters. First the final supplier invoices, then artist settlements, then crew expenses and sometimes a refund round for visitors. That means many actions in very little time. In that phase, mistakes are rarely spotted early.

The EU Instant Payments Regulation makes verification of the payee more important across Europe. In the euro area, payment service providers must offer a name and account check before a transfer is confirmed from 9 October 2025. The Netherlands already had an IBAN-Name Check in practice, but the European rule makes this type of control broader and more consistent. The European Commission explains the instant payments rules, including payee verification.

Where event payments go wrong

Event payments often involve temporary collaborations. A supplier sends an invoice from a holding company while the contract uses a trade name. An artist manager sends a last-minute message with a new account number. A crew member still uses an old account name from a previous season.

Those are not edge cases. They are normal event operations.

Practical rule: verify payment details when someone is onboarded, not when the payment batch is already waiting.

A team that is careless here usually creates three problems at once:

- Delayed payouts because payments have to be corrected manually

- More pressure on support and finance because recipients start asking where their money is

- Higher fraud risk when a fake invoice or changed IBAN slips through

If a fraud case does occur, the discussion rarely stays operational. Liability, duty of care and evidence quickly become relevant. Background on legal support in bank fraud cases can help teams understand how such conflicts may be assessed.

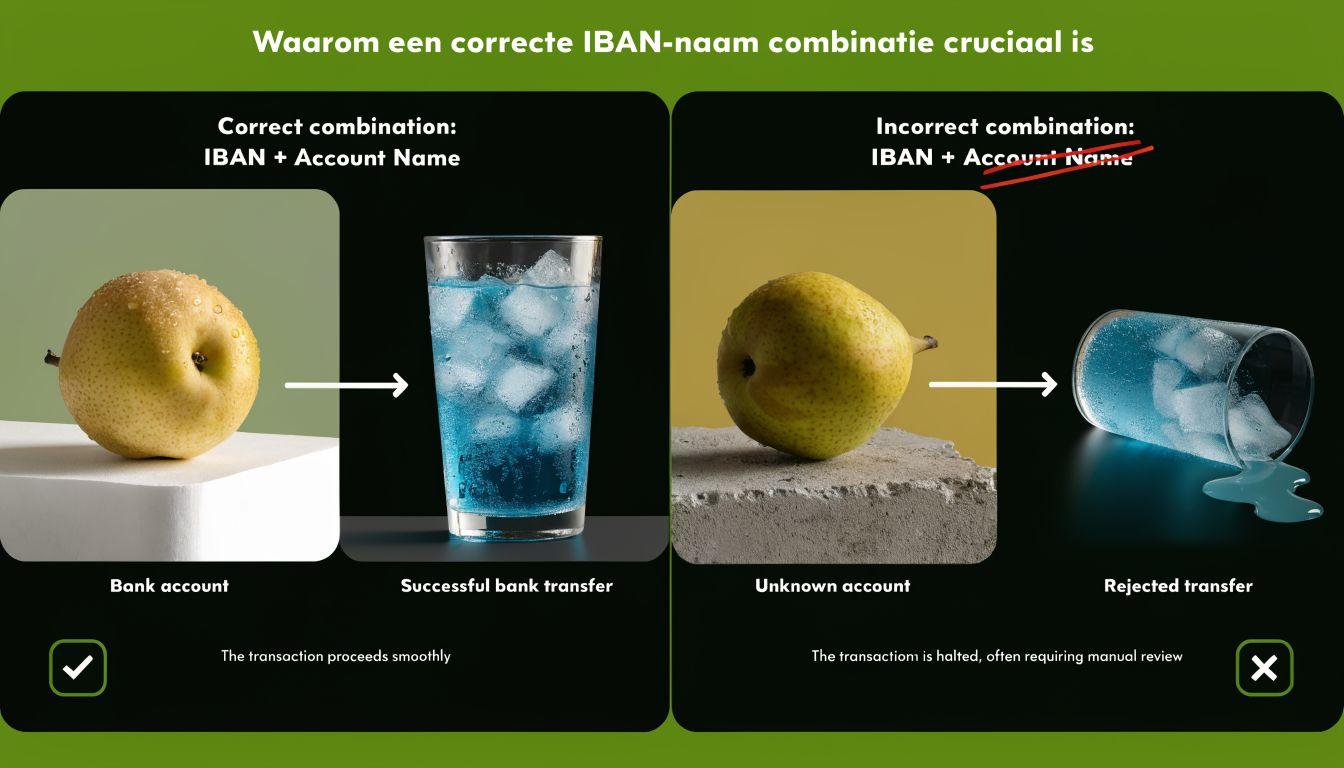

Why a name check does more than IBAN validation

Plain IBAN validation only confirms that the account number can exist. It does not prove that the account belongs to the right party. That is exactly why the name check matters. It addresses the risk event organizers often face: payments that look administratively correct on paper, but cannot be defended operationally or legally.

Refunds add another layer. Visitors expect speed, but speed without verification can create more recovery work later. A good name check does not slow the process down. It prevents one small error from becoming an expensive correction.

The basics: the automatic IBAN-name check at your bank

For a single transfer in a banking app or online banking environment, the check usually happens automatically. While the payer enters the name and IBAN, the payer's bank compares those details with the receiving bank. A result appears before the payment is confirmed.

In practice, the result is usually one of these:

| Result | Meaning | Action |

|---|---|---|

| Match | Name and IBAN correspond | Continue as normal |

| Close match | Small spelling difference or abbreviation | Check against contract or known records |

| No match | Name does not fit the account number | Pause payment until verified |

| Cannot be checked | The control cannot be completed | Confirm manually through a trusted channel |

A match is the green signal. A close match deserves attention. A missing company suffix or small spelling difference can be harmless, but only when the surrounding context makes sense.

A no match should be treated as a red flag. Not as a technical inconvenience, but as a payment stop until someone verifies what is happening. That is especially important when an invoice includes a new account number.

Business and bulk verification methods

The standard bank check works well for individual transfers. For events, that is often not enough. An organization paying suppliers, freelancers, venues, artists and visitors rarely works with one transaction at a time. Bulk verification becomes an operational requirement.

| Method | Best for | Speed | Cost indication |

|---|---|---|---|

| Company registry check alongside bank details | New business suppliers and service providers | Medium | Internal time |

| Bulk check through a portal or bank file | Large payout and refund batches | High | Depends on tool and volume |

| EUR 0.01 test payment | Exceptions and doubtful cases | Low | Very low, but manual |

For business payments, the account name should logically match the contracting party. Many differences are not fraud, but administrative noise: a trade name on the proposal and a legal name on the bank account. This control is most useful during onboarding, not on the day money has to leave.

For larger files, a specialized solution is more practical. Betaalvereniging Nederland explains how the IBAN-Name Check helps prevent mistakes and fraud. For organizers who want to centralize their payout process, it is better to avoid loose manual banking work and use a fixed workflow for payouts in an event platform.

Bulk checks work best before exporting to the bank, not after a batch has already been submitted.

A watertight financial process for your event

Many teams only verify details when payment is due. That is exactly when pressure is highest and the margin for error is smallest. A solid process moves verification forward, so the payment run itself becomes predictable.

For event operations, this is not a side issue. It affects cash flow, supplier relationships and support workload. Banks such as ABN AMRO explain how name checks help prevent wrong payments, but the organizer remains responsible for its own process.

A strong workflow starts when data is collected:

- Onboarding with fixed fields

Collect official name, IBAN, contract name and invoice details in one standard form. - Verification before the first payment

Run the name check as soon as a new party enters the system. - One source of truth

Store only verified payment details in a central administration. - Four-eyes control for changes

Any changed IBAN shortly before payment deserves additional review.

Working rule: a last-minute change to payment details never goes straight into the same batch without extra verification.

Refunds need their own rhythm. Use payment data from the original transaction wherever possible, validate exceptions in bulk and place no-match cases in a separate worklist. At higher volumes, settlement, CRM and communication need to connect well. See also more transparency in settlement and payment releases.

Privacy and legal attention points

Some organizers wonder whether checking an IBAN by name fits within GDPR. The concern is understandable, but the bank check is deliberately limited. It does not share balances, transaction history or other sensitive account information. The relevant question is only whether the name and IBAN combination is sufficiently consistent. A practical Dutch manual on the privacy context is available from Quantaris.

That does not remove the organizer's own responsibility. Payment data stored internally still has to be managed carefully. Access should be limited, changes should be traceable and old spreadsheet exports should not keep circulating.

For a wider review of customer data, access rights and data ownership, clear policy around GDPR and data ownership in an event CRM is just as important as the bank check itself.

FAQ about IBAN verification

Can a bank block a payment after a no match?

Usually not automatically. The bank warns the payer, but responsibility remains with the person or organization making the payment. Rabobank explains how name checks on payment files can reveal mismatches before submission.

What should an organizer do with a close match?

Treat it as a control point. A small spelling difference can be harmless, but supplier and artist payments should always be checked against contracts or known company details.

Does this work for bulk refunds?

Yes, if the workflow is designed for it. For larger refund rounds, bulk verification is better because mismatches become visible at once instead of during manual processing.

Is a no match always fraud?

No. It can also be an old account name, a typo or a difference between trade name and legal name. Operationally, that does not change the first step: payment should stop until the mismatch is explained.

In short: no verified name-IBAN combination, no payout. Professional event operations need more than ticket sales alone. A tight process for refunds, payouts, CRM and settlement prevents errors before they become support tickets or fraud cases.